Deemed exports play a crucial role in India’s Goods and Services Tax (GST) system, significantly impacting economic growth and trade efficiency. As of April 2023, over 13 million businesses are registered under GST, showcasing its extensive adoption and inherent complexity. Familiarizing yourself with the concept and implications of deemed exports is essential for businesses to navigate the complexities of GST effectively.

Let’s get into the benefits and applications of deemed exports within the GST framework.

Meaning of Deemed Exports and Their Significance

Deemed exports refer to the supply of specific goods manufactured in India to a domestic buyer, yet they are treated as exports for tax purposes.

This government initiative offers a win-win situation, incentivizing domestic manufacturing and boosting export competitiveness.

Here’s why understanding deemed exports is crucial:

- Tax Advantages: Unlike zero-rated exports (meaning no GST is levied), deemed exports initially attract GST. However, you can claim a refund of the paid tax, improving your cash flow and reducing tax burdens.

- Enhanced Global Competitiveness: Deemed exports allow you to participate in international tenders and compete with foreign suppliers on a more level playing field. Tax benefits translate to lower costs for your products, making them more attractive in the global marketplace.

Eligibility Criteria and Conditions for Deemed Exports

Now that you’ve grasped the essence of deemed exports let’s enter the eligibility criteria. It is a checklist to ensure your business qualifies for these tax benefits.

Meeting the Government’s Nod:

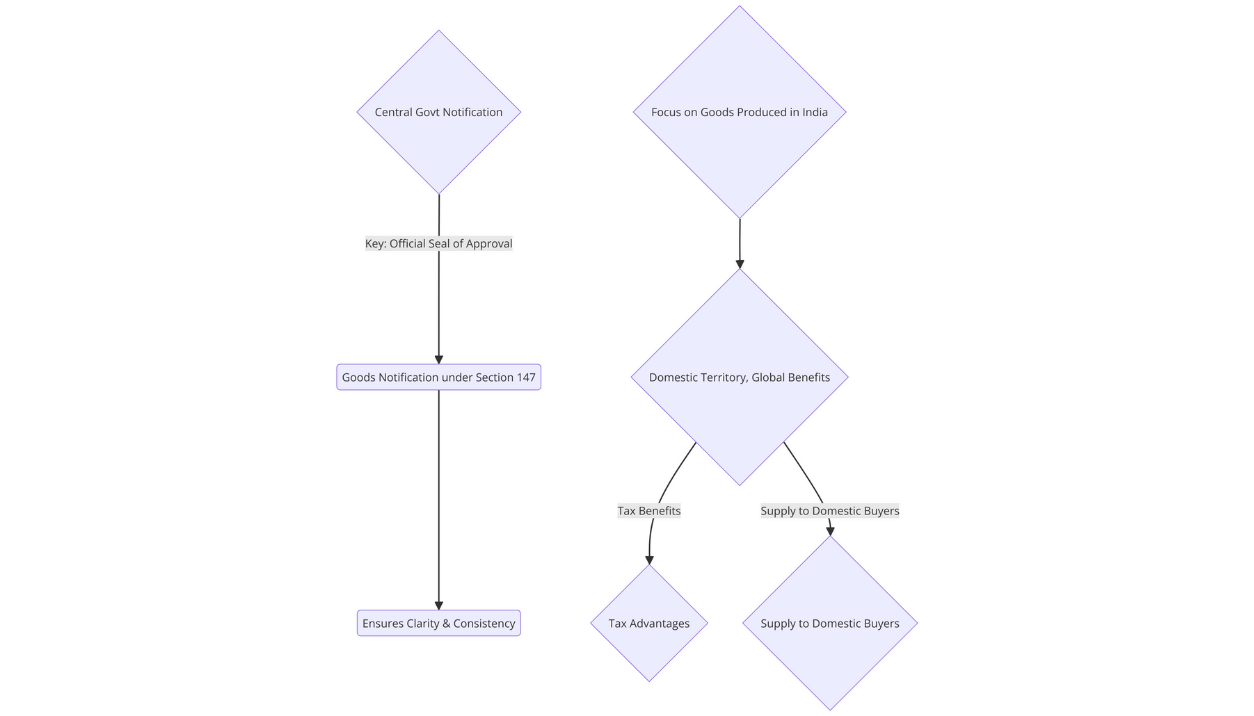

Central Government Notification: The key lies in the official seal of approval. Deemed exports are only recognized if the Central Government notifies the specific goods you supply under Section 147 of the Central Goods and Services Tax (CGST) Act. This ensures clarity and consistency across the system.

Focus on Goods: Here’s a crucial distinction—deemed exports solely apply to the supply of goods produced in India. Businesses dealing in services won’t be able to leverage this scheme.

Domestic Territory, Global Benefits: The beauty of deemed exports is that the goods you supply never have to leave Indian soil. They can be sold to domestic buyers yet enjoy the tax advantages typically associated with exports.

Production and Payment Protocols:

Made in India: Your goods must be manufactured or produced within India to qualify as deemed exports. This promotes domestic production and strengthens the Indian manufacturing sector.

Currency Flexibility: When it comes to payment, you have options. You can receive payment in Indian Rupees (INR) or any other convertible foreign currency. This caters to the diverse needs of international business transactions.

Bond-Free Transactions: Deemed export supplies cannot be made under a Letter of Undertaking (LUT) or a bond. These are instruments used in regular exports, and deemed exports have distinct regulations.

GST and Refunds: You’ll be required to pay the applicable GST on deemed exports at the time of supply. However, the good news is that you can claim a full refund of this paid tax. This eases cash flow concerns and incentivizes participation in the scheme.

Adhering to these criteria can unlock the potential of deemed exports and elevate your business to a competitive edge in the global marketplace.

In the next section, we’ll explore the different categories of supplies that qualify as deemed exports under GST!

Also Read: Top International Freight Forwarding Companies in Delhi

Categories and Examples of Deemed Exports

Now that you’ve aced the eligibility criteria let’s explore the exclusive club, which consists of supplies that qualify as exports under GST.

Remember Notification No. 48/2017 – Central Tax, issued in 2017, as your key reference point. It outlines the specific supplies that enjoy this beneficial status.

Here are some prominent examples:

Export-Oriented Production:

Advance Authorization (AA): If you supply goods to a company holding an AA license, you’re eligible for deemed export benefits. The government grants these licenses to promote export-oriented manufacturing.

Export Promotion Capital Goods Authorization (EPCG): Supplying capital goods to entities with an EPCG authorization also qualifies as a deemed export. This scheme encourages businesses to invest in machinery and equipment for export production.

Supplies to Export-Oriented Units (EOUs) and Similar Setups: Export-Oriented Units (EOUs), Software Technology Parks (STPs), and other special economic zones are hubs for export-focused businesses. Supplying goods to these units qualifies as deemed exports.

Gold:

Supply of Gold by Banks or PSUs against AA: When a bank or Public Sector Undertaking (PSU) supplies gold against an Advance Authorization, it’s considered a deemed export. This caters to the specific needs of the gold export industry.

Understanding the Nuances:

The definition of deemed exports under the Foreign Trade Policy (FTP) and the GST law differ slightly. It’s always advisable to consult with a qualified tax professional for the most up-to-date information specific to your situation.

Also Read: Freight Forwarding Companies in Pune

Tax Implications and GST Rates for Deemed Exports

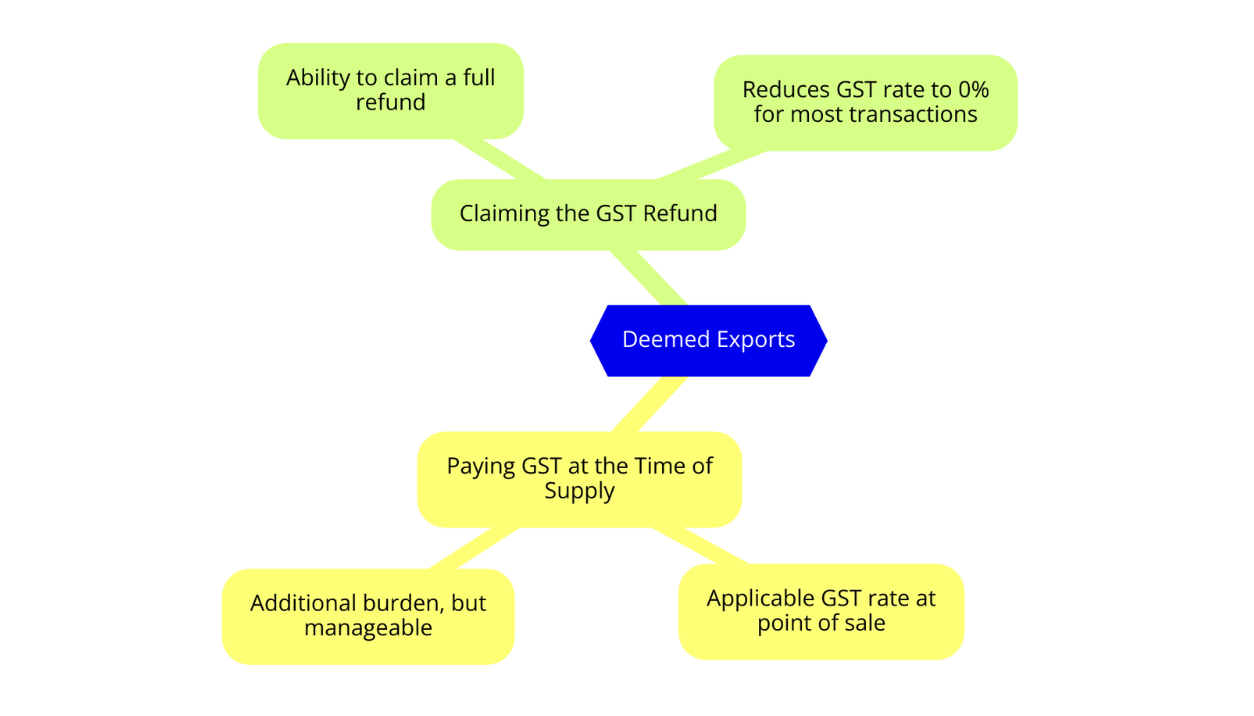

The tax treatment of deemed exports might seem counterintuitive at first. Unlike regular exports that are zero-rated (meaning no GST is levied upfront), deemed exports involve a two-step process:

- Paying GST at the Time of Supply: You’ll be required to pay the applicable GST rate on the deemed export transaction at the point of sale. This might seem like an additional burden, but fret not!

- Claiming the GST Refund: The beauty of deemed exports lies in the ability to claim a full refund of the paid GST. This reduces the applicable GST rate to 0% for most deemed export transactions.

Understanding the Exceptions:

While a 0% GST rate applies in most scenarios, there might be specific situations where a nominal GST rate is levied on deemed exports. It’s crucial to consult with a tax advisor to determine the exact rate applicable to your business case and the notified category under which your deemed export falls.

How to Manage Deemed Export Transactions?

Now that you’ve grasped the tax implications let’s get into the practicalities of managing deemed export transactions. Here’s a roadmap to navigate the process smoothly:

Prior Intimation (for Specific Cases):

Prior intimation is required for deemed export transactions involving specific categories of recipients. This ensures transparency and streamlines the refund process.

Here’s a breakdown:

- EOU/EHTP/STP/BTP Units: If you’re supplying goods to a recipient unit like an Export Oriented Unit (EOU), Export House Electronic Technology Park (EHTP), Software Technology Park (STP), or Bio-Technology Park (BTP), they must provide prior intimation.

- This intimation is filed in Form A, informing you, the supplier, and the relevant GST authorities about the details of the goods being procured.

- The Development Commissioner must pre-approve Form A for the transaction to proceed.

Record-Keeping and Submissions

You must maintain meticulous digital records for all your deemed export transactions. These records form the backbone of your refund claim:

- Detailed Documentation: Maintain comprehensive records of invoices, bills of lading (for applicable scenarios), and any other documents that support the transaction’s deemed export nature.

- Monthly Submissions: Don’t forget to electronically submit your GST return every month, reflecting the deemed export supplies and the tax paid on them.

Tailored Procedures: Suppliers vs. EOUs/EHTPetc.:

The specific procedures for claiming deemed export refunds might differ slightly depending on whether you’re a supplier or the recipient unit (EOU, EHTP, etc.). Here’s a quick breakdown:

For Suppliers:

1. Once you’ve supplied the goods and received payment, you can issue a tax invoice to the recipient unit.

2. Ensure the recipient unit endorses the tax invoice and acknowledges receipt of the goods.

3. Submit a copy of the endorsed invoice and your refund application to the relevant GST authorities.

4. Prepare a detailed statement outlining the invoice-wise breakdown of the deemed export supplies.

5. Obtain an acknowledgment from the recipient unit’s tax officer (EOU, etc.).

6. Submit all the required documents electronically to claim your refund.

For EOUs/EHTP/STP/BTP Units:

1. File Form A, as mentioned earlier, to initiate the process.

2. Upon receiving the goods and the tax invoice from the supplier, endorse the invoice and send a copy back to the supplier.

3. Cooperate with the supplier to provide the necessary documentation for their refund claim.

Following these steps and maintaining proper documentation, you can easily navigate the deemed export refund process, unlocking the tax benefits and propelling your business toward tremendous export success!

GST Refund Procedure for Deemed Exports

Understanding the process for claiming refunds on GST paid for deemed exports is crucial for maximizing the benefits of this scheme. Here, we’ll unpack this process’s rules, conditions, and steps.

Applicable Rules and Amendments

The Central Goods and Services Tax (CGST) Rules govern the process for claiming deemed export refunds. These rules are subject to amendments, so staying updated with the latest regulations is advisable.

Who Can Claim the Refund?

Not everyone involved in a deemed export transaction can claim a refund. Here’s a breakdown of eligibility:

- Suppliers: If you are the supplier of the goods and have paid GST on the deemed export transaction, you can claim the refund.

- Recipients (Limited Cases): In specific scenarios, the recipient unit (like an EOU) might be eligible to claim the refund. However, this is not the general rule.

Required Documents and Evidence

A robust application backed by proper documentation is key to a smooth refund process. Here are the essential elements:

- Refund Application (Form RFD-01): File this form electronically on the GST portal. It captures crucial details about your refund claim.

- Supporting Documents: Attach copies of invoices, bills of lading (if applicable), and any other documents that substantiate the nature of the deemed export transaction.

- Detailed Statement: Prepare a comprehensive invoice-wise breakdown of the deemed export supplies and the GST paid on each.

- Endorsed Invoice (for Suppliers): If you’re a supplier, ensure you have a copy of the tax invoice endorsed by the recipient unit, acknowledging receipt of the goods.

- Tax Officer Acknowledgment (for Suppliers): Obtain an acknowledgement from the recipient unit’s tax officer for your records.

Online Filing for Convenience

The recommended approach is to file your deemed export refund claim electronically on the GST portal. This offers a faster and more transparent process. The portal guides you through the steps, ensuring all necessary information is captured.

Manual Option (If Needed):

In exceptional cases, you can file a manual refund application. However, this is generally discouraged due to potential delays and complexities. Always prioritize online filing for a smoother experience.

By adhering to these guidelines and maintaining meticulous documentation, you can confidently navigate the deemed export refund process and maximize the benefits available under this scheme.

Documentation and Compliance

While the potential benefits of deemed exports are enticing, ensuring proper documentation and compliance is paramount. This section will equip you with the knowledge to navigate this aspect effectively.

Critical Documents for Deemed Export Transactions and GST Compliance

For a seamless deemed export experience, here’s a list of essential documents you’ll need to maintain:

- Tax Invoice: This serves as the official record of the transaction. Ensure it includes details like GSTINs (Goods and Services Tax Identification Numbers) of both parties, the HSN (Harmonized System Nomenclature) code of the goods, and the value of the supply.

- Prior Intimation Form (if applicable): For deemed export transactions involving EOUs, EHTPs, STPs, or BTPs, Form A, filed by the recipient unit, is crucial for initiating the process and obtaining pre-approval.

- Endorsed Tax Invoice (for Suppliers): When claiming a refund, suppliers must have a copy of the tax invoice endorsed by the recipient unit, acknowledging receipt of the goods.

- Detailed Statement: Prepare a comprehensive document outlining the invoice-wise breakdown of deemed export supplies and the corresponding GST paid on each transaction.

- Tax Officer Acknowledgment (for Suppliers): Obtain an acknowledgement from the recipient unit’s tax officer for your records. This strengthens your refund application.

- Supporting Documents: Maintain copies of any additional documentation that bolsters your claim, such as bills of lading (for applicable scenarios) or communication records with the recipient unit.

Declarations for Refund Success:

Both recipients and suppliers play a role in the refund process through declarations:

- Recipient Declaration (for Specific Cases): In specific scenarios where the recipient unit (like an EOU) claims the refund, a declaration stating they haven’t claimed Input Tax Credit (ITC) on the deemed export transaction is mandatory.

- Supplier Declaration: Suppliers typically declare that they haven’t supplied the goods under a bond or Letter of Undertaking (LUT) and that they’ll utilize the refunded amount for the intended purpose.

Transparency Through GSTR Filings:

Your GST return filings (GSTR-1 and GSTR-3B) play a crucial role in transparency:

- GSTR-1: In this outward supply return, you’ll need to disclose details of all deemed export transactions, including the recipient’s GSTIN, HSN code, and the value of the supply.

- GSTR-3B: This consolidated return requires you to reflect the total tax liability on deemed export transactions and the total ITC claimed on purchases related to these transactions (if any).

Remember, this is a general overview. Specific requirements might vary depending on the nature of your deemed export transaction and the notified category under which it falls. Consulting a tax advisor ensures you stay compliant with the latest regulations.

By maintaining meticulous documentation and adhering to these disclosure practices, you can confidently demonstrate compliance and navigate the deemed export process.

Also Read: Top Freight Forwarding Companies in India 2024

Conclusion

Understanding the complexities of deemed exports under GST is crucial for businesses aiming to maximize tax benefits and streamline operations. Deemed exports provide a unique opportunity to enhance competitiveness by enabling refunds on GST paid, fostering a healthier cash flow, and supporting domestic manufacturing.

Partnering with a reliable logistics company like Intoglo can be a game-changer. Intoglo offers seamless door-to-door shipments from India to the USA. Our expertise in handling international shipments, experience across multiple industries backed with advanced technology, and dedicated customer support make Intoglo an invaluable partner in your business journey.

Explore the advantages of working with Intoglo and how our tailored logistics solutions can help you navigate the complexities of deemed exports and beyond. Visit Intoglo today to learn more about our services and how we can support your business’s growth and success.

Leave a comment